DocFusion

With ever evolving legislation, banks need to must reduce regulatory operating costs and eliminate the cost of non-compliance without impacting time to market. This combined with mounting security risks, operational inefficiency, rising expectations and the need to drive down operational costs, makes the challenge even more formidable.

Competition with nimble new Fintech companies is disrupting the industry and is causing some banks to create a parallel IT infrastructure which is costly and unnecessary. Over 65% of IT projects in banks will fail against their initial promises and over 50% of all the IT projects will fail to ever create shareholder value. Shadow IT costs are on the rise with employees striving to use the newest and greatest products and tools.

While we all understand that traditional banks need to improve across the board and that becoming digital is a prerequisite for success, this does not mean ditching legacy systems and procuring and implementing a whole new IT landscape. Nobody will disagree that Cloud has increased compute power and that the processing of Big Data and AI can provide massive benefit, however the real battle ground is on the face of the Customer.

Todays customers are less worried about cost than having a frictionless omnichannel experience. Retail banking, corporate banking, wealth management, loans and mortgage processes all need a massive transformation to provide hyper personalized customer service at scale.

At their core, banks need to maximise emphatic customer experience with workflow driven processes and dynamic rules which simplify and expedite the banking experience for all customers.

Will Covid-19 signal the end of the bank branches or personalized business banking? Nobody really knows the answer to this question, but one thing is sure; a seamless digital, personalized, efficient and remote customer experience is the key to survival, not to success. Not withstanding this, Covid-19 has changed the world and how we perceive things forever. Some companies have given their employees the right to work from home forever.

Against the backdrop of the above, I am sure that you will be shocked to hear that according to research firm Forrester, over 70% of business processes are paper and email based. Document templates are stored in multiple locations and can be as primitive as multiple people’s hard drives. This flouts with risk and compliance and causes havoc for internal content owners such as legal, marketing, technical and other corporate content owners.

This results in customers receiving unprofessional digital or paper documentation with outdated logo’s, styling and legal terms and often has the customer print documents, fill them in manually, scan and return to sender. Equally upsetting to customers is that the bank has is not prepopulated their information, and often omnichannel communications are chaotic.

In addition to this, new customers and customers looking at additional products are faced with a plethora of manual documents that are time consuming, unprofessional, and sloppy.

These were the problems that legacy systems such as SAP, SalesForce and others were supposed to solve. In reality, while these systems are great at optimizing internal processes, but when it comes to processes that are non-standard or which cross organizational boundaries they are found lacking. This is the gap that Document Automation and Generation fills.

The need for banks to unleash commercial innovation and maintain a competitive edge, through rapid time to market, customer obsession and operational excellence, is not a holy grail but an achievable ambition.

Banks need to begin with the question of, “What does being digital really mean?”. Document Generation and Automation, combined with Smart Workflow and Digital Signatures is a step in the right direction. Banks must stop trying to bend legacy systems into something they were never designed to be, while also avoiding throwing the baby out with the proverbial bath water.

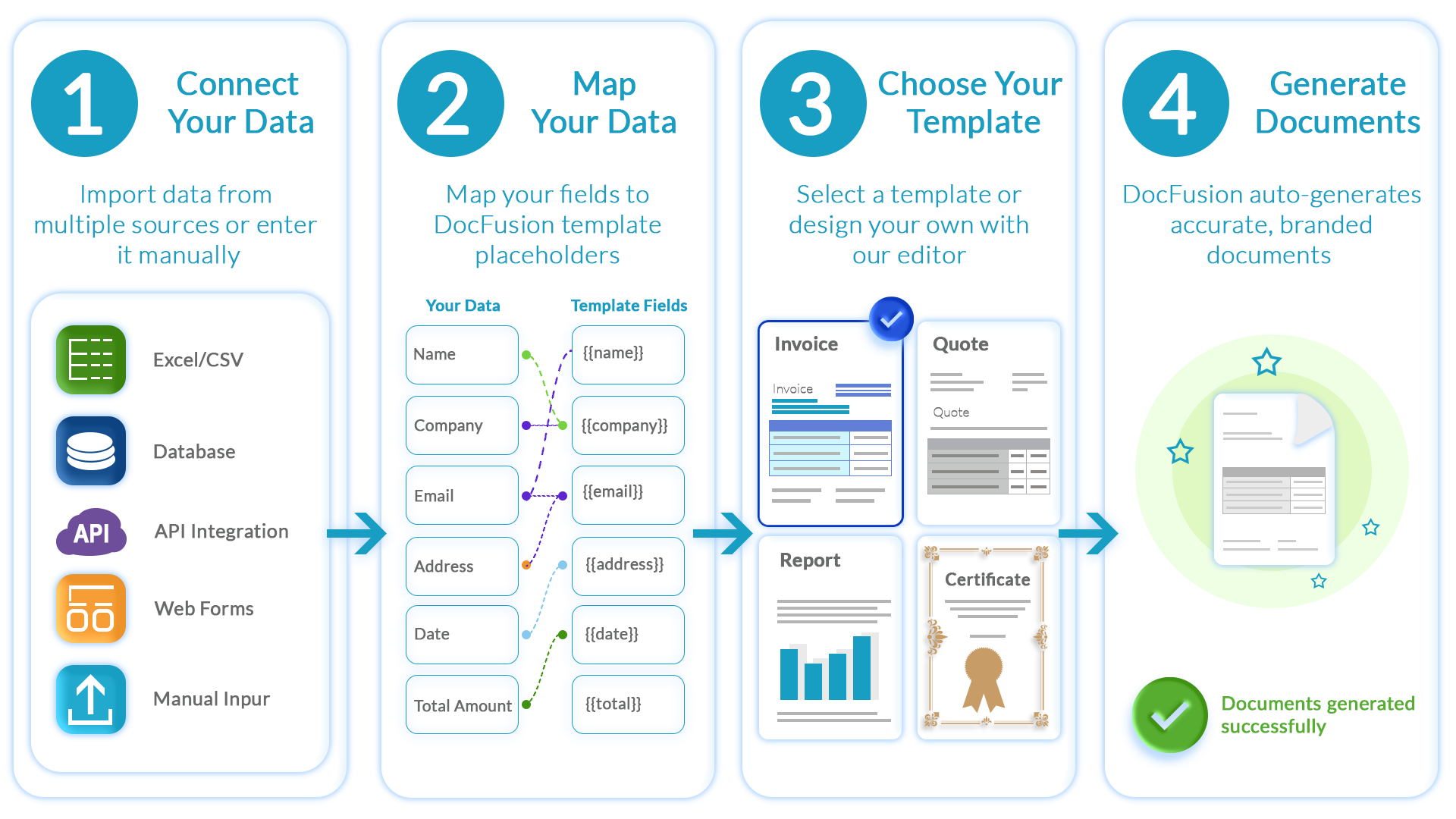

Any Document Automation and Generation system must have the following attributes:

- It must have an easy to use Forms component.

- It must provide workflow competency or integrate into the clients flexisting workflow system

- It must provide digital signatures.

- It must provide or integrate back into the clients DMS.